Introduction

So, you’re getting ready to enroll in Medicare, something you’ve paid into your entire working life. But here’s something the government doesn’t exactly shout from the rooftops: a single, innocent mistake in that process can trigger devastating penalties for the rest of your life. Imagine your monthly Medicare bill suddenly being 10%, 20%, or even 40% higher than your neighbor’s—not for one year, but forever. This isn't a scare tactic; it’s a financial reality for millions who stumble into traps they never saw coming. For every 12 months you delay enrollment the wrong way, you could be hit with a 10% penalty on your Part B premiums for life. We’re going to show you exactly how to avoid that.

Section 1: The Three Most Dangerous Penalty Traps

When we talk about Medicare penalties, we're not talking about one-time fees. These are permanent hikes to your monthly premiums that you’ll pay for as long as you have your coverage. Let's walk through the three biggest penalty traps we see people fall into every day and, more importantly, the exact steps to sidestep them.

Trap #1: The Part B Enrollment Window Mistake

The first and most common trap is misunderstanding your Part B enrollment timeline. Part B is your medical insurance—think doctor visits, outpatient care, and medical supplies. Most people get a seven-month window to sign up for it, known as the Initial Enrollment Period, or IEP. This period kicks off three months before the month you turn 65, includes your birthday month, and wraps up three months after.

Now, here’s where things go wrong. A lot of people think, "I'm healthy, I don't need it yet," or "I'll just sign up when I retire." They let that seven-month window slam shut without doing anything. If that's you, and you don’t have other specific, qualifying health coverage, you are walking right into the Part B late enrollment penalty.

And it’s a tough one. The penalty adds 10% to your standard Part B premium for each full 12-month period you could've had Part B, but didn't. This isn’t a one-and-done fine. It’s a permanent surcharge you will pay for the rest of your life.

Let’s translate that into real money for 2026. The standard Part B premium is $202.90 per month. If you delay signing up for just two years without a valid reason, you’re looking at a 20% penalty. That means an extra $40.58 will be tacked onto your bill every single month. Your premium would be $243.48 instead of $202.90—for life. Over 20 years, that’s almost $10,000 extra for the exact same coverage.

The Solution: Know Your Enrollment Period.

The fix is simple but critical: you have to enroll during your seven-month Initial Enrollment Period unless you have a specific exception. The main one is if you're still working and have health coverage through your or your spouse's employer, and that employer has 20 or more employees. If that’s your situation, you can delay Part B without a penalty.

Once you stop working or that employer coverage ends, you’ll get what's called a Special Enrollment Period, or SEP. This gives you an eight-month window to sign up for Part B without getting hit with the late penalty. The clock on those eight months starts ticking the month after your employment or your coverage ends, whichever comes first. Don't miss that window.

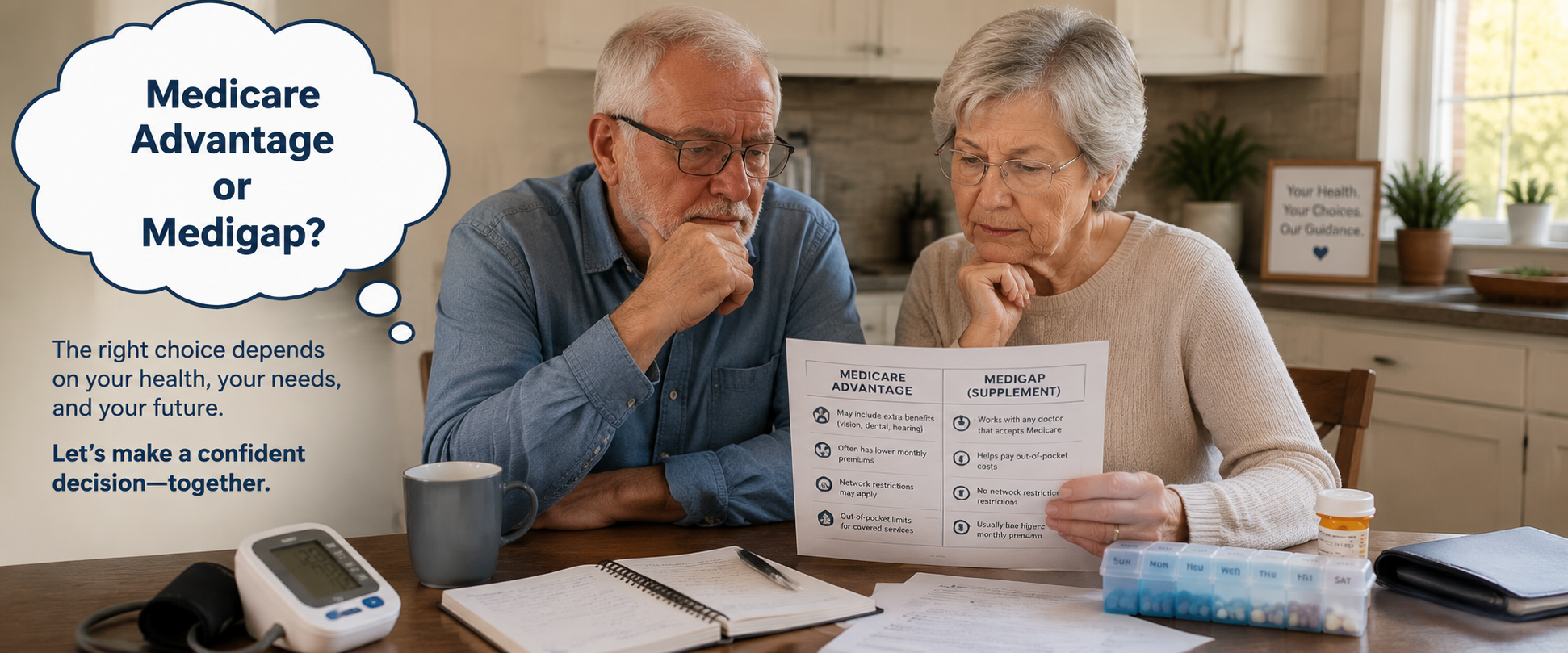

Trap #2: The Employer Coverage and COBRA Misunderstanding

This leads us right into the second trap, which is hands-down one of the most misunderstood and financially painful rules in all of Medicare: what actually counts as "creditable coverage." So many people assume any health insurance gives them a free pass to delay Medicare. That is a catastrophic mistake.

There are two huge misunderstandings here. First, the size of your employer is everything. If you work past 65 and get health insurance from a company with *fewer* than 20 employees, Medicare is considered your primary insurer. Your work plan is secondary. If you fail to sign up for Part B when you turn 65 in this scenario, your employer’s plan might pay little to nothing for your medical bills, and you'll get slammed with that late penalty later. The 20-employee rule is non-negotiable.

The second, and even more common error, involves COBRA. When you leave a job, you're often offered COBRA to continue your health coverage. It feels like a safety net. But here’s the brutal truth: Medicare does NOT consider COBRA to be creditable coverage for delaying Part B.

Let me say that again because it is so important: COBRA will not protect you from the Part B late enrollment penalty. If you’re eligible for Medicare and you choose COBRA instead of signing up for Part B, that penalty clock starts ticking the second you lose your active employer coverage. Countless people ride out their 18 months of COBRA, only to get a shocking notice that they now have a 10% or higher lifetime penalty when they finally enroll in Medicare.

The Solution: Verify Your Coverage is "Creditable" for Part B.

The only kind of coverage that lets you safely delay Part B is a group health plan from an employer with 20 or more employees, and it must be based on current, active employment—either yours or your spouse's. Retiree health plans don't count. VA benefits alone won't let you delay Part B without penalty. Marketplace (A C A) plans don't count.

If you're working past 65, have a chat with your HR department. Ask them directly, "Is our health plan considered creditable coverage for Medicare Part B?" and confirm the company has more than 20 employees. If you're leaving a job, remember your eight-month Special Enrollment Period starts right away, even if you take COBRA. Don't count on COBRA to save you.

Trap #3: The Part D "Pay Later" Penalty

The third major trap is the Part D prescription drug penalty. A lot of people turning 65 think, "I don't take any pills, so I don't need a drug plan. I'll just get one later if I need it." This is another expensive mistake.

Medicare requires you to have some form of "creditable" prescription drug coverage as soon as you're eligible. If you go for 63 continuous days or more without it, you'll trigger the Part D late enrollment penalty. And just like the Part B penalty, this one is for life.

The Part D penalty is calculated as 1% of the "national base beneficiary premium" for every full month you went without coverage. For 2026, that base premium is about $38.99. So for each month you wait, you add about $0.39 to your future monthly premium. If you wait five years—that's 60 months—you're looking at a 60% penalty. That’s an extra $23.40 tacked onto your drug plan's premium every single month, forever. And because the base premium can change each year, your penalty amount can go up, too.

The Solution: Enroll in a Part D Plan or Have Other Creditable Drug Coverage.

To avoid this, you either need to enroll in a Medicare Part D plan during your Initial Enrollment Period or make sure you have other creditable drug coverage. Unlike Part B, many other types of drug coverage are considered creditable for Part D, including coverage from the VA, TRICARE, or many employer and union plans.

Your current plan is required to mail you a letter every year telling you if its drug coverage is "creditable." Hang on to those notices. If you don't have other creditable drug coverage, the safest and often cheapest move is to enroll in the lowest-cost Part D plan in your area. Think of it as a low-cost insurance policy against a lifelong penalty. You can always switch plans during the Annual Enrollment Period each fall if your prescription needs change.

CTA: Call to Action

Trying to keep all these rules straight can feel like a lot, and it's way too easy to make a mistake. To help you stay on track and make sure you've covered all your bases, we’ve put together a free "Medicare Penalties Checklist." It’s a simple guide that walks you through these exact traps and helps you pinpoint your personal enrollment deadlines.

Section 2: How to Fight and "Void" a Penalty

Okay, but what if it's too late? What if you've already gotten that dreaded letter from Social Security telling you that you owe a lifelong penalty? You might feel like your hands are tied, but that's not always the case. While there’s no magic "void" button, you have the right to appeal the penalty through a process called reconsideration.

The best shot you have at a successful appeal is proving you had qualifying creditable coverage during the time in question. For instance, maybe you *did* have coverage from a large employer, but there was a paperwork mix-up and Medicare's records are wrong.

Here are the steps to appeal a Part B penalty:

- File the Appeal—Fast: You usually have just 60 days from the date on the penalty letter to file your appeal. Don't let that deadline pass.

- Use the Right Form: You'll need to fill out a "Request for Reconsideration" form, which is SSA-561-U2. You can get this directly from the Social Security Administration.

- Gather Your Evidence: This is the most important step. You need proof. Dig up letters from your old HR department, old insurance cards, or even tax forms showing you paid for a group health plan. The more documentation, the better.

- Submit Your Appeal: Mail the completed form and copies of all your evidence to the address listed right on your penalty notice.

For a Part D penalty appeal, the process is similar but handled by a different group. The notice you get will give you instructions on how to file an appeal with Medicare's independent review contractor.

The bottom line is this: if you believe the penalty was a mistake, you have to fight it. Many people get their penalties removed because they can prove they had the right coverage all along.

Conclusion

The Medicare world is full of tricky rules that can easily lead to permanent financial penalties. But by understanding these three major traps, you can take control of your enrollment and do it with confidence.

Just remember the big three:

First, know your seven-month Initial Enrollment Period for Part B and get it done inside that window.

Second, understand that only active group coverage from a large employer (20+ employees) lets you safely delay Part B. COBRA is a trap.

And third, lock in a Part D plan when you're first eligible—unless you're 100% sure you have other creditable drug coverage—to dodge that lifelong prescription penalty.

Getting your Medicare enrollment right is one of the most important financial decisions you'll make for your retirement. Don't let a simple misunderstanding drain thousands of dollars from your savings.

If you're still feeling unsure about your unique situation, here is our "Medicare Penalties Checklist" And if you found this helpful, please subscribe and share it with a friend who’s also getting close to Medicare age. You could save them from a lifetime of costly mistakes. Thanks for watching.

Medicare Penalties Checklist

- [ ] Define Your Initial Enrollment Period (IEP): It lasts seven months—three months before your 65th birthday, the month of your birthday, and three months after.

- [ ] Evaluate Part A Coverage: If you or your spouse worked 10+ years (40 quarters) and paid Medicare taxes, Part A is free. If not, you may face a 10% premium penalty for twice the years you delayed.

- [ ] Verify Part B "Creditable" Coverage: If you are still working at 65+ and have employer coverage, you may delay Part B. COBRA and retiree plans are generally not considered creditable coverage.

- [ ] Check Part D Drug Coverage: If you go 63 days or more without "creditable" prescription drug coverage (like VA, TRICARE, or a qualified employer plan), you will incur a permanent 1% penalty based on the national base premium ($38.99 in 2026).

- [ ] Utilize Special Enrollment Periods (S E P): If you had active employer coverage, you have 8 months to sign up for Part B after the employment or coverage ends (whichever comes first) without penalties.

• [ ] Appeal if Necessary: If you received a penalty but had creditable coverage, you can file a request for

reconsideration with your plan.